Credit Scores in 2026 Matter: What Clear Lake Families Need to Know Right Now

It’s April 2026, and if you haven’t checked your credit report in the last six months, you might be looking at a completely different landscape than you remember. For families in the Clear Lake and Bay Area, the "old rules" of credit have been tossed out the window. If you’re planning on buying a home near the NASA Parkway or looking to upgrade to a bigger lot in League City, the way lenders look at your financial DNA has undergone a massive transformation.

The credit game changed late last year when Fannie Mae and other major players fundamentally shifted how they evaluate borrowers. We aren’t just looking at a three-digit number anymore; we’re looking at your life’s financial patterns.

The Death of the "620 Floor"

For decades, the "620 FICO score" was the magic number. If you were below it, you were essentially locked out of conventional mortgages. If you were above it, you were in the game. But as of 2026, that hard cutoff has been blurred.

Lenders are now moving toward more sophisticated models like VantageScore 4.0 and FICO 10T. Why does this matter to a Texas family? Because these models use "trended data." Instead of a single snapshot of your debt today, they look at your behavior over the last 24 months. They want to see if you’re paying down your balances or if you’re slowly digging a deeper hole.

"In my years of helping Texas families navigate the credit trail, I’ve never seen a shift this significant. The doors are opening for more families, but you still need a map to walk through them. It’s no longer about a quick fix; it’s about proving your financial character over time." , William Avery, Owner of Texas Credit Trail.

Why Clear Lake Families are Benefiting (and Struggling)

The new 2026 standards are a double-edged sword. On one hand, approximately 5 million people who were previously "unscorable" or had "thin files" are now getting a fair shake. On the other hand, the complexity of these new models means that small mistakes can have a larger, lingering impact than they used to.

The Good News: Your "Invisible" Payments Now Count

If you’ve been diligently paying your rent in the Bay Area, keeping your lights on with Reliant, and paying your AT&T bill on time, you finally have an advantage. The 2026 models now incorporate alternative data:

- Rental History: Consistent on-time rent payments are now a primary factor in mortgage approvals.

- Utility & Phone Bills: Your everyday reliability is finally being rewarded.

- Cash Flow Analysis: Lenders can now look at your banking history to see how you manage the money you actually have, not just the money you owe.

The Bad News: "Trended Data" Doesn't Forget

In the old days, you could pay down a credit card balance 30 days before applying for a loan and see a quick spike in your score. In 2026, the FICO 10T model sees right through that. It looks at your average balance over the last two years. If you’ve been maxed out for 23 months and just paid it off, the model knows you’re a higher risk than someone who has consistently kept their utilization low.

The Cost of Waiting: A Reality Check

Many families think, "I’ll just wait until next year to fix my credit." But in the 2026 economy, waiting is the most expensive decision you can make. While the 620 "floor" is gone, the "interest rate gap" has widened.

Consider a typical $400,000 home loan in the Houston area. A family with an "Excellent" score might secure a rate that is 1.5% lower than a family with a "Fair" score. Over a 30-year mortgage, that 1.5% difference translates to over $100,000 in extra interest payments. That is money that should be going toward your children’s college funds or your retirement, not to a bank’s bottom line.

If you want to see where you stand, our education page breaks down these factors in even more detail.

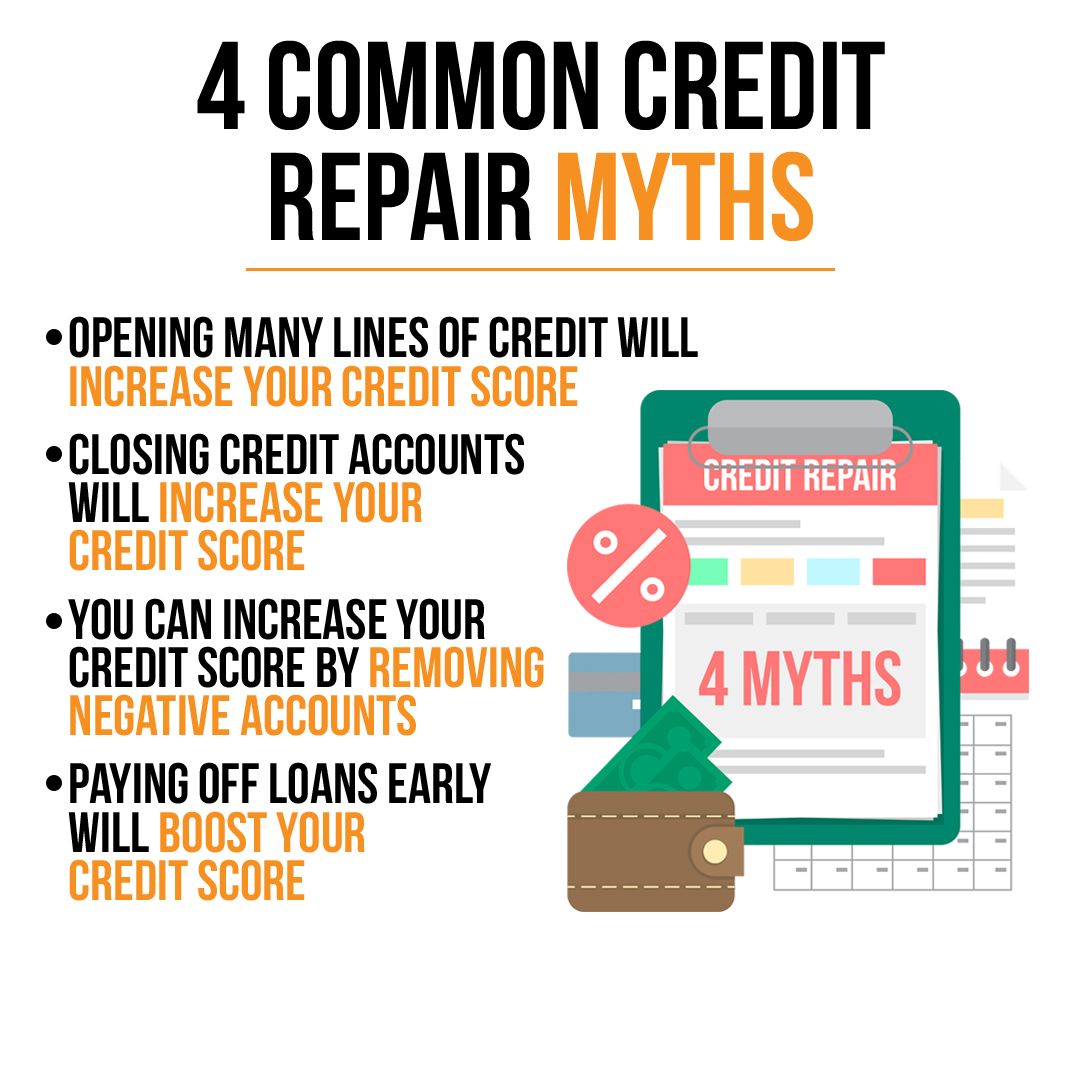

Common 2026 Credit Myths

As an expert in the field, I hear the same misconceptions every day. Let’s clear the air for our Texas neighbors:

- Myth: "I should close my old accounts to clean up my report."

- Reality: Closing accounts actually hurts you. It shortens your credit history and reduces your available credit, which spikes your utilization ratio.

- Myth: "Checking my own score will lower it."

- Reality: Checking your own score is a "soft inquiry" and has zero impact. In fact, in 2026, not monitoring your score is a recipe for identity theft disasters.

- Myth: "I can fix it all myself with a template letter I found online."

- Reality: The credit bureaus have integrated advanced AI to flag "template" disputes. If you don't use a professional, custom approach, your disputes are likely to be ignored or labeled "frivolous."

Who This Information Is For (And Who It Isn't)

This guide is specifically for Texas families who are tired of being told "no." If you are a hard-working parent in Clear Lake trying to get into a better school district, or a young professional in the Bay Area looking to buy your first condo, this is for you. You need to know that the system has changed, and you need to adapt.

This is not for people looking for "hacks" or illegal "Cis" (Credit Privacy Numbers). We don't do gimmicks at Texas Credit Trail. We focus on real, lasting services that build a foundation for your family’s future.

How to Navigate the Trail in 2026

If you're feeling overwhelmed, don't be. Credit is a tool, not a death sentence. Here is the path we recommend for our neighbors:

- Audit Your Report: Don't just look at the score. Look at the data. Are there old collections from 2020 still hanging around? Are there late payments that aren't actually yours?

- Address the "Big Three": Payment history, amounts owed, and length of history still make up the bulk of your score. Focus here first.

- Leverage Your Rent: Make sure your landlord or property management company is reporting your on-time payments to the bureaus.

- Get Professional Eyes on It: Sometimes you're too close to the problem to see the solution. A professional review can identify "low-hanging fruit" that can boost your score faster than you think.

The Texas Credit Trail Difference

We aren't a giant, faceless corporation based in a skyscraper in New York. We are based right here in Texas, and we understand the local economy. We know that life happens: medical bills, job transitions, and family emergencies can all knock your credit off the rails.

Our goal is to educate first. We want you to understand why your score is what it is, and then give you the tools to change it. Whether you're looking at our ebooks for a DIY start or you need our full-service team to handle the heavy lifting with the bureaus, we are here to guide you.

The "Trail" isn't always easy, but it's always worth it. When you finally get the keys to that new house or drive that new truck off the lot with a low-interest loan, you'll know the work paid off.

"Education is the greatest equalizer in the financial world. Most people aren't 'bad with money'; they just haven't been taught how the system actually works. Our job is to pull back the curtain." : William Avery.

Bottom Line

The credit environment of 2026 is more flexible, but it's also more data-hungry. Clear Lake families have a massive opportunity to use their everyday bills to build a legacy, but they have to be proactive. Procrastination is a debt that pays no dividends.

If you’re ready to stop guessing and start growing, let’s get to work. You don't have to wander the credit trail alone.

Take the first step toward a stronger financial future for your family today.

Click here to book your consultation and start your credit journey now.

Ready to Start Your Credit Journey?

Get personalized credit repair guidance from William Avery

Book Free Consultation