How Long Do Late Payments Stay on Your Report? The Simple Trick to Improve Your Score Right Now

We’ve all been there. Life in Texas moves fast, between keeping up with the rising property taxes, the kids’ school schedules, and the everyday hustle, it’s easy for a bill to slip through the cracks. You open your mail, and there it is: a late notice. Suddenly, your heart sinks. You start wondering if that one missed payment is going to haunt your dreams of buying a home or a new truck for the next decade.

The short answer? A late payment stays on your credit report for seven years.

But before you panic, I want to tell you something the big banks don't usually broadcast: not all late payments are created equal, and there is a "simple trick" (well, a few of them) that can help you mitigate the damage right now. At Texas Credit Trail, we believe in empowering our neighbors with the truth about how credit actually works, so you can stop stressing and start building.

The Reality of the Seven-Year Rule

Under the Fair Credit Reporting Act (FCRA), most negative information, including late payments, can stay on your credit report for up to seven years from the date the account first became delinquent.

However, the clock doesn't start from the day you realized you forgot to pay. It starts from the Original Delinquency Date. This is the date of the very first missed payment in a series that led to the account being late.

Here’s the breakdown of how lenders see those "late" marks:

- 30 Days Late: This is the first threshold. Most creditors won't even report you to the bureaus until you are a full 30 days past the due date.

- 60 Days Late: The damage increases. Lenders start to see you as a higher risk.

- 90+ Days Late: This is a major red flag. It signals to lenders that you may be heading toward a default or a charge-off.

Why Payment History is the "Big Kahuna"

To understand why a late payment hurts so much, you have to look at the "pie" of your credit score. Payment history accounts for 35% of your total FICO score. It is the single most influential factor in determining whether you’re a "Prime" borrower or someone who gets stuck with high-interest rates.

As you can see in the graphic above, that 35% chunk (the red section) is the foundation of your financial reputation. When you miss a payment, you aren't just missing a bill; you’re chipping away at the largest pillar of your score.

The "30-Day Secret" Most Texans Miss

Here is a bit of "insider info" that saves our clients a lot of headaches: If you are only 10 or 15 days late, your credit score is usually safe.

While the credit card company or the bank might hit you with a late fee the day after your due date, they generally do not report that lateness to the three major credit bureaus (Equifax, Experian, and TransUnion) until you hit the 30-day mark.

"Most people think a single day of lateness ruins their credit. The truth is, you usually have a 30-day window to fix the mistake before the credit bureaus ever hear about it. Use that window wisely." , William Avery, Owner of Texas Credit Trail

If you realize you've missed a payment, don't wait for the next billing cycle. Pay it immediately. If you get it in before that 30-day window closes, your credit report will still show "Paid as Agreed."

The Simple Trick: The "Goodwill Adjustment"

If you’ve already crossed that 30-day line and the late payment is sitting on your report like a dark cloud, there is a strategy that works surprisingly well, yet most people never try it. It’s called a Goodwill Letter.

This isn't a legal dispute. It’s a human-to-human request. If you have been a loyal customer for years and this was a one-time slip-up (maybe you were moving, or there was a family emergency), you can write to the creditor and ask for a "Goodwill Adjustment."

The logic is simple: You aren't saying the report is wrong; you’re asking them to remove the negative mark as a courtesy because of your otherwise stellar history. In the competitive financial landscape of Texas, many banks would rather keep a loyal customer happy than lose them over one 30-day late mark.

How to write a Goodwill Letter:

- Be Polite: Don't demand. Ask nicely.

- Take Responsibility: Acknowledge that you missed the payment.

- Explain the "Why": Briefly mention the circumstances (job change, illness, etc.).

- Highlight Your Loyalty: Mention how long you've been a customer.

- Ask for Removal: Specifically ask them to report the account as "Paid as Agreed" to the bureaus.

While this doesn't work every time, it's a powerful "trick" that can see a late payment vanish in weeks rather than years.

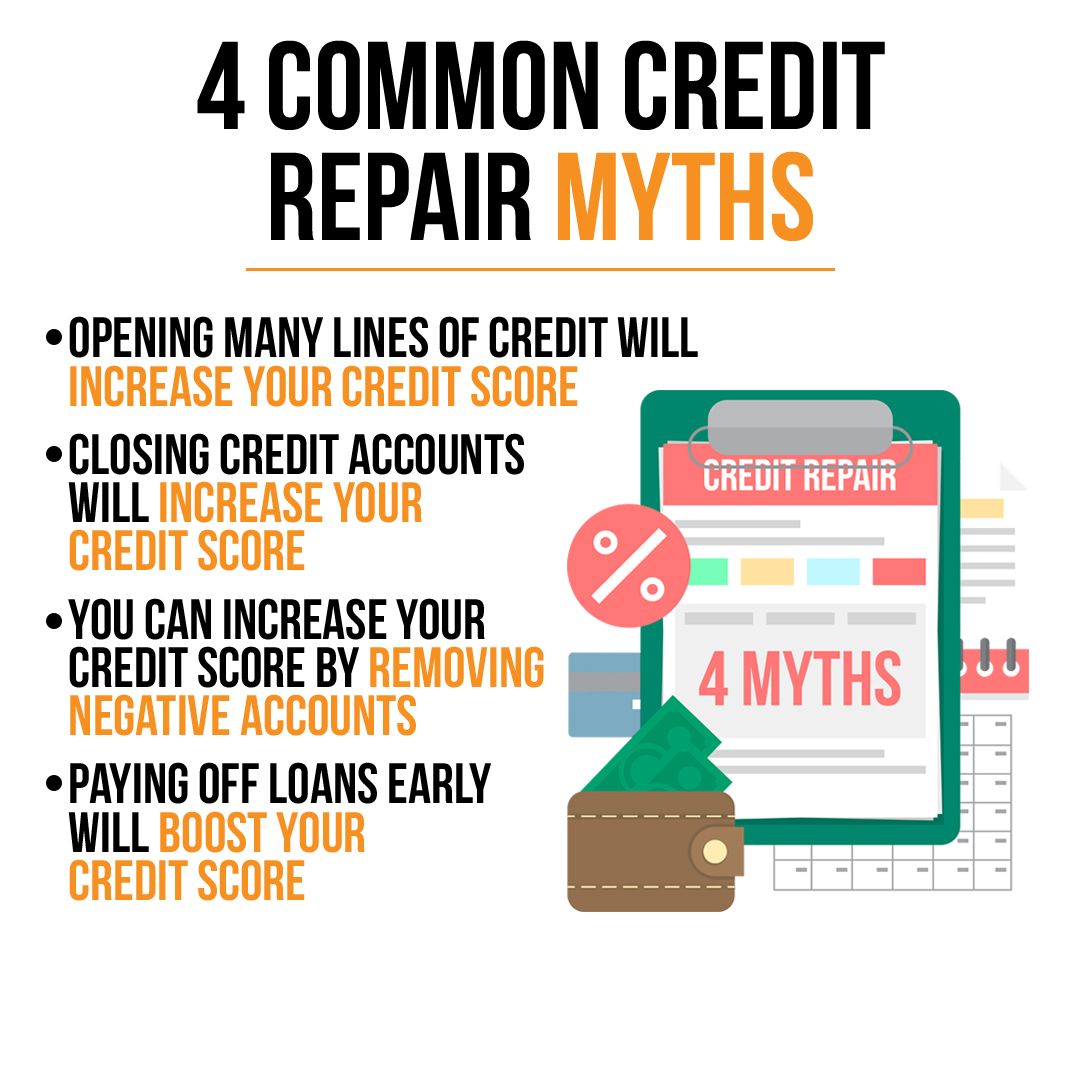

Myths vs. Reality: What Actually Works?

There’s a lot of bad advice floating around the internet. You might hear people say you can just "dispute everything" and it will all disappear. That's not how it works. At Texas Credit Trail, we focus on Education because knowing the difference between a myth and a strategy can save you thousands in interest.

As shown above, many common beliefs, like the idea that paying off a late debt immediately removes it from your history, are simply not true. Paying the debt is essential to stop further damage, but it doesn't automatically delete the historical record of being late. That’s where professional strategy comes into play.

How the Impact Fades (The "Diminishing Effect")

Here is the good news for Texas families: the impact of a late payment is not permanent. While the mark stays for seven years, its "weight" on your score drops significantly over time.

A 30-day late payment from three years ago hurts much less than a 30-day late payment from last month. As the negative mark gets older, your more recent "on-time" payments start to carry more weight. This is why we tell our clients that even if we can't get a specific mark removed immediately, we can still help you build a positive history that eventually outshines the old mistakes.

Navigating the Texas Financial Landscape

In Texas, your credit score affects more than just your ability to get a loan. Because our state has a deregulated electricity market and a competitive insurance landscape, your credit score can actually dictate how much you pay for your lights and your car insurance.

A single late payment can lead to:

- Higher security deposits for utilities.

- Increased premiums for auto and home insurance.

- Denied applications for rental properties in high-demand areas.

The cost of inaction is real. If a late payment is dragging your score down by 50 points, you could be paying hundreds of extra dollars every month in "hidden" credit costs.

Steps to Rebuild Starting Today

If you’re looking at your report and seeing late payments, here is your game plan:

- Check for Errors: Is that late payment actually yours? Was it really 30 days late? If there’s a factual error, you have the legal right to dispute it. Check our E-books for more on how to spot these errors.

- Set Up Autopay: Never let a "oops, I forgot" moment happen again. Even setting up autopay for the "minimum amount due" can save your credit score.

- Lower Your Utilization: If you can’t remove the late payment, offset its impact by paying down your credit card balances. This lowers your "Amounts Owed," which is 30% of your score.

- Become an Authorized User: Ask a family member with a perfect payment history to add you as an authorized user on their oldest card. You'll inherit their "on-time" history, which helps dilute the impact of your late payment.

When Information Isn’t Enough: The Professional Advantage

What we’ve covered here is the foundation. For many Texas families, knowing the "7-year rule" and the "Goodwill Trick" is a great start. But let’s be honest: life gets in the way. Dealing with creditors, writing letters, and tracking credit bureau responses is a full-time job.

Technically, you can do all of this yourself. But there’s a reason people hire professionals. We know the specific language that creditors respond to. We know how to navigate the complicated bureaucracy of the credit reporting agencies. Most importantly, we have the experience of seeing thousands of reports and knowing exactly which lever to pull to get the fastest results.

"We give you the tools for free because we believe in education first. But when you’re ready to see real, accelerated change without the headache of doing it alone, that’s where Texas Credit Trail steps in." : William Avery

Bottom Line: Don't Let the Past Dictate Your Future

A late payment is a speed bump, not a brick wall. Whether it happened during a tough month or was just a simple oversight, you have the power to fix it. Seven years might be the legal limit, but with the right strategy, you can minimize its impact much sooner.

If you’re ready to stop guessing and start growing, we’re here to help. Check out our current offers or contact us today for a consultation. Let’s get you back on the trail to a score you can be proud of.

Ready to Start Your Credit Journey?

Get personalized credit repair guidance from William Avery

Book Free Consultation