7 Mistakes You’re Making with Texas Credit Repair (and How to Fix Them Before Buying Your Next Bay Area Home)

Buying a home in the Bay Area or Clear Lake isn't just about finding the right layout or a backyard big enough for a Texas-sized smoker. It’s a financial marathon. If you’ve been eyeing a property near the water or a quiet street in League City, you already know the stakes: interest rates are the gatekeepers. A difference of 50 points on your credit score can mean the difference between a comfortable monthly payment and a mortgage that eats your entire paycheck.

Many Texas families realize their credit isn't quite "mortgage-ready" and jump headfirst into credit repair. I see it every day at Texas Credit Trail. Folks have the best intentions, but without a map, they end up taking two steps back for every step forward. Credit repair isn't just about removing the "bad stuff"; it’s about understanding the "Trail" of your financial habits.

If you are a Texas family ready to stop renting and start owning, this is for you. If you’re just looking for a "magic wand" to make legitimate debts disappear overnight, you might be in the wrong place. We believe in education and real results through strategy.

Here are the seven most common mistakes I see Texans making with their credit repair and exactly how to fix them before you sit down with a loan officer.

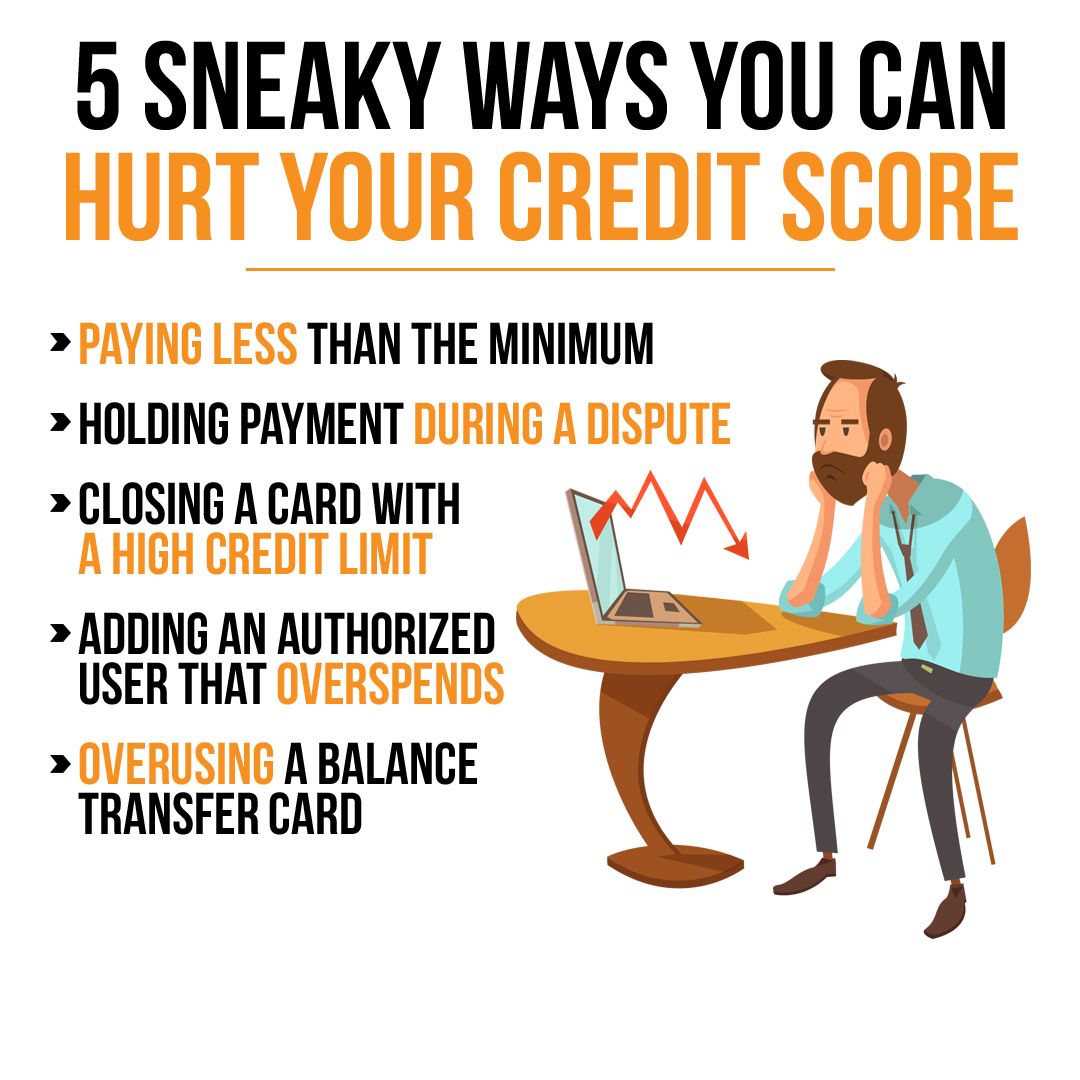

1. Closing Old Credit Cards After Paying Them Off

It feels good to pay off a balance and "cut the cord," doesn't it? You think you're clearing the deck. In reality, you might be sinking your own ship.

The Mistake: When you close an old account, you instantly shorten your "Length of Credit History" and potentially spike your "Credit Utilization Ratio."

The Fix: Keep those old accounts open. If there’s no annual fee, let the card sit in a drawer. If you’re worried about inactivity, put one small subscription: like your Netflix or a car wash pass: on it and set it to autopay.

As you can see in the chart above, your "Length of Credit History" accounts for 15% of your total score. If you close a card you’ve had for ten years, your average age of accounts drops, and so does your score. Leave the old accounts alone; they are the foundation of your credit trail.

2. Disputing Accurate Negative Items Without a Strategy

There’s a myth floating around the internet that if you just dispute everything on your report 50 times, the bureaus will eventually get tired and delete it.

The Mistake: This is what we call "shotgunning" disputes. When you dispute accurate information without a legal basis or a specific error to point to, the credit bureaus (Equifax, Experian, and TransUnion) can flag your disputes as "frivolous." Once you’re flagged, getting them to look at a real error later becomes much harder.

The Fix: Focus on accuracy. Look for incorrect dates, wrong balances, or accounts that aren't yours. Texas Credit Trail teaches that credit repair is a scalpel, not a sledgehammer. You need to identify specific violations of the Fair Credit Reporting Act (FCRA).

"The hard truth is that credit bureaus aren't your friends, but they have to follow the law. If you don't know the law, you're just throwing paper at a wall and hoping it sticks. You need a strategy that focuses on consumer rights, not just repetitive guessing." : William Avery, Owner of Texas Credit Trail.

3. The "Pay-and-Pray" Method with Collections

You get a tax refund or a bonus at work, and you decide to pay off that old $400 medical bill from three years ago. You pay it, wait a month, and… your score goes down.

The Mistake: Many older credit scoring models (the ones most mortgage lenders still use) see a "paid collection" as a recent activity. By paying it without a "Pay for Delete" agreement, you essentially "wake up" the debt, making it look like a brand-new negative event on your timeline.

The Fix: Never pay a collection agency without getting a written agreement that they will remove the entry from your credit report entirely upon payment. This is called a "Pay for Delete." Without that piece of paper, you’re just giving away money and potentially hurting your score right before you apply for a home loan.

4. Applying for New Credit While in the "Repair Zone"

I see this often: a family is working hard to clean up their past, but then they see a "0% interest for 24 months" deal on a new sofa or a truck they think they need for the move.

The Mistake: Every time you apply for credit, a "Hard Inquiry" hits your report. If you’re in the middle of credit repair, your score is sensitive. Multiple inquiries signal to lenders that you are "credit hungry" or in financial distress.

The Fix: Freeze your spending. If you are within six months of buying a home in the Bay Area, do not open a new credit card, do not finance furniture, and for heaven's sake, do not buy a new car. Wait until you have the keys to your new front door in your hand.

5. Maxing Out Your "Credit Builder" Secured Cards

Secured cards are a great tool for building credit from scratch. We often recommend them for the next generation of Texas homeowners. But they can be a double-edged sword.

The Mistake: If you have a secured card with a $300 limit and you spend $250 on groceries, your utilization is at 83%. Even if you pay it off in full every month, the balance reported to the bureaus makes it look like you’re maxed out.

The Fix: Follow the "30% Rule": or better yet, the "10% Rule." On a $300 card, never let the balance exceed $30-$90. High utilization accounts for 30% of your score. You can be the most responsible payer in Texas, but if your cards are near their limits, your score will stay in the basement.

6. Ignoring New Monthly Due Dates

It sounds simple, but life gets busy. Between work and the kids' soccer practice, a 30-day late payment can slip through the cracks.

The Mistake: A single 30-day late payment can tank a 700-score by 100 points or more instantly. When you are in the process of credit repair, you cannot afford a single "fresh" late payment. It’s like trying to dry off while you're still standing in the rain.

The Fix: Set every single bill to "Minimum Payment Autopay." Even if you plan to pay more, the autopay ensures you are never "late" in the eyes of the credit bureaus. Payment history is the biggest factor in your score (35%). Check your services to ensure you have a monitoring system in place that alerts you to any missed steps.

7. Paying Upfront Fees to "Gurus" Who Promise the World

Texas law is very specific about credit repair. If a company tells you they can "guarantee" a 100-point jump in 30 days, or if they ask for a massive upfront fee before doing any work, walk away.

The Mistake: Falling for "Fast-Track" scams. In Texas, credit services organizations must be registered and often need to maintain a $10,000 surety bond to protect consumers. Many "out-of-state" internet gurus don't follow these rules.

The Fix: Work with a local, transparent partner. At Texas Credit Trail, we focus on the about us values: neighborly service, educational digital guides, and a clear path forward. We don't use "magic." We use the law and financial literacy.

Why This Matters for Your Bay Area Home Search

The real estate market around Clear Lake and the Bay Area is competitive. When a "Good" or "Excellent" score (as shown in the chart above) hits a lender's desk, you get the "fast pass." You get lower down payment options and interest rates that save you tens of thousands of dollars over thirty years.

If you make these seven mistakes, you aren't just hurting your score; you're delaying your family's future. You’re staying in that rental for another year while home prices continue to climb.

The Bottom Line

Credit repair isn't a DIY weekend project like painting a fence. It's a strategic process of correcting the past while building a solid future. You've worked hard for your family, and you deserve a credit score that reflects that hard work.

Don't let a few avoidable mistakes stand between you and your next home. Whether you're just starting your credit journey or you're trying to fix a few bumps in the road, there is a clear trail to follow.

Stop guessing and start growing your score today.

Click here to Book Your Credit Evaluation and Start Your Trail to Homeownership

Ready to Start Your Credit Journey?

Get personalized credit repair guidance from William Avery

Book Free Consultation