How to Build Credit from Scratch in Texas: 5 Steps for the Bay Area’s Next Generation

If you’re a young adult living in the Clear Lake or Bay Area, or a parent trying to set your kids up for success, you’ve likely realized that "cash is king" isn't the whole story anymore. It’s 2026, and your credit score is essentially your financial passport. Whether you’re looking to lease an apartment near the NASA Johnson Space Center, buy your first truck, or eventually settle down in a home in Friendswood, that three-digit number determines how much you’ll pay: or if you’ll get approved at all.

Starting from scratch can feel like a "catch-22." You need credit to get credit, right? Not exactly. At Texas Credit Trail, we’ve spent years helping Texas families navigate the maze of the credit bureaus. We know the insider tricks that the big banks don't always advertise. Building a 700+ score from zero isn't a mystery; it’s a process.

This guide is specifically for the next generation of Texans who have no credit history yet. If you already have a "thin file" or a score that’s seen better days, this is for you too. If you’re looking for "overnight" miracles or live outside of the Lone Star State, our methods might not be the right fit. We focus on sustainable, educational growth for our neighbors right here at home.

The Reality of "No Credit" in 2026

Having no credit is often just as frustrating as having bad credit. In the eyes of a lender, a "ghost" file represents an unknown risk. In an economy where data is everything, being a ghost means higher deposits for utilities, higher insurance premiums, and higher interest rates.

"The biggest mistake I see young Texans make is waiting until they need credit to start building it. By then, it’s usually too late to get the best rates. You don’t build a trail while you’re already lost in the woods; you map it out before you leave the house." : William Avery, Owner of Texas Credit Trail

Here is the 5-step roadmap to building a rock-solid credit foundation from the ground up.

Step 1: Start with a Controlled "Toolbox"

You can’t build a house without tools. To build credit, you need a reporting account. For most beginners in the Bay Area, this means looking at secured credit cards or credit-builder loans.

A secured credit card works by you providing a deposit: say $200: which then becomes your credit limit. Because you've provided the collateral, the bank takes zero risk. However, they report your usage to the credit bureaus just like a "real" card.

Alternatively, credit-builder loans are a fantastic Texas secret. Instead of getting the money upfront, your payments are held in a locked savings account while the lender reports your "on-time payments." Once the loan is paid off, you get the cash back plus a boost to your score.

Step 2: The 35% Rule (Never Miss a Date)

If there is one thing you remember from this post, let it be this: Payment history is the single most important factor in your credit score. It accounts for a massive 35% of the total calculation.

In the digital age, there is no excuse for a late payment. One single 30-day late mark can tank a beginner's score by 100 points instantly. Set up "Auto-Pay" for the minimum balance on every account you open. Even if you plan to pay the full balance manually, that auto-pay safety net ensures you never miss a reporting cycle.

Whether you're finishing up at San Jacinto College or starting your first job in the Houston medical district, life gets busy. Automate your financial life so your credit grows while you sleep.

Step 3: Master the "Utilization" Trick

Most people think that as long as they pay their bill by the due date, they’re doing fine. But there’s a hidden trap: Credit Utilization. This is the ratio of how much credit you’re using compared to your limit.

If you have a secured card with a $300 limit and you spend $290 on gas and groceries, your utilization is 96%. Even if you pay it off the next day, the credit bureau might see that high balance and think you're over-extended.

The Pro Tip: Keep your reported balance under 10% for maximum points, or at least under 30% to stay in the "safe" zone. If your limit is $300, don't let more than $30 show up on your monthly statement. You can use the card more, just pay it down before the statement closing date.

Step 4: The "Piggyback" Method (Authorized Users)

For many Texas families, the fastest way to jumpstart a young person's credit is through an Authorized User status. If a parent or relative has a long-standing credit card with a perfect payment history and a high limit, they can add the "Next Gen" family member as an authorized user.

The beauty of this is that the older account’s history often "mirrors" onto the younger person's credit report. Suddenly, an 18-year-old can have five years of perfect payment history overnight.

Note of caution: This only works if the primary cardholder is responsible. If they miss a payment, it could hurt your score too. This is a strategy built on trust and education.

Step 5: Diversify Your Trail

Lenders like to see that you can handle different types of debt. This is called your "Credit Mix." Once you have a credit card established for 6–12 months, you might consider a small installment loan or a different type of revolving credit.

Don't go out and buy a car you can't afford just to "build credit." That’s a trap. Instead, look at small, manageable ways to show variety. This could be a retail card for a store you already shop at or a small personal loan for a necessary expense.

Remember, every time you apply for new credit, a "hard inquiry" hits your report, which can temporarily dip your score. Be strategic: don't apply for five things at once. Space them out by at least six months.

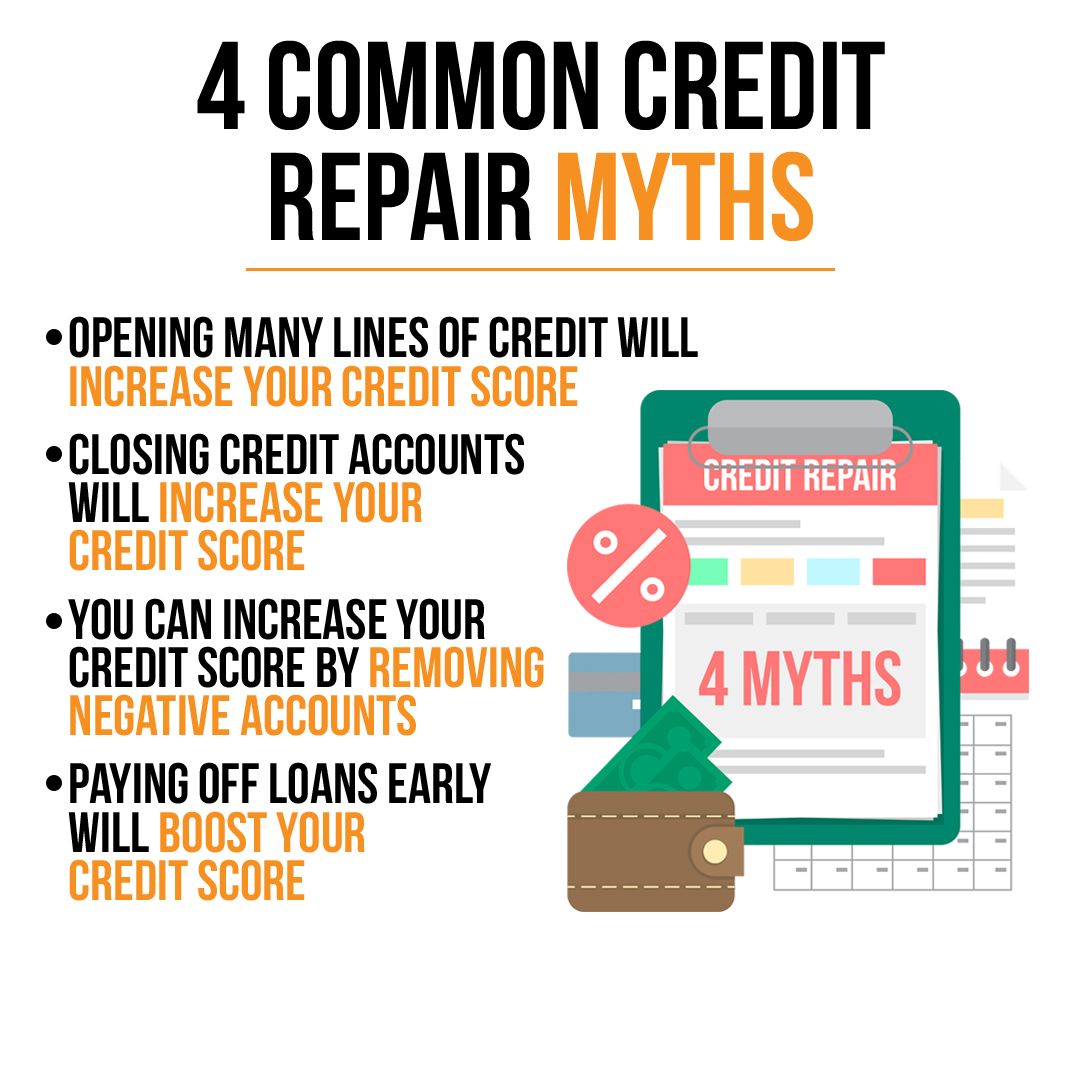

Common Myths That Trip Up Texans

We hear a lot of misinformation at Texas Credit Trail. Let’s clear the air:

- "Carrying a balance helps your score." WRONG. You do not need to pay interest to build credit. Paying in full every month is the smartest move.

- "Checking your own score hurts it." WRONG. Using apps or your bank’s portal to check your score is a "soft pull" and has zero impact.

- "Closing old accounts helps." WRONG. The length of your credit history matters. Keep those early accounts open, even if you don't use them often.

The Cost of Waiting

In the Bay Area, the difference between a "Fair" credit score and an "Excellent" credit score can equate to tens of thousands of dollars over a lifetime.

- On a car loan: You might pay 4% interest with great credit vs. 18% with no credit.

- On a mortgage: A 1% difference in interest rates can cost you $100,000+ over 30 years.

Building credit is a marathon, not a sprint. The steps above will put you on the right path, but managing the nuances of credit reports and dealing with the bureaus can be a full-time job.

Why Professional Guidance Matters

While the DIY steps above are the foundation, the credit industry is designed to be confusing. Errors on credit reports are incredibly common, and the bureaus aren't always quick to fix them. If you’re a Texas family looking to ensure your graduate or young professional starts their life with the best possible financial footing, you don't have to go it alone.

At Texas Credit Trail, we specialize in taking the "thin files" and "no-credit" situations and turning them into success stories. We provide the services and the digital guides necessary to navigate the specific landscape of the 2026 financial world.

Don't let a lack of history hold back the next generation of our community. Let’s get your trail started the right way.

Ready to build a legacy of strong credit for your family?

Click here to book your consultation and start your credit journey today!

Ready to Start Your Credit Journey?

Get personalized credit repair guidance from William Avery

Book Free Consultation